Jet2 tops UK airline resilience rankings as aviation fuel costs remain elevated — new data shows significant differences in how well popular carriers are protected this summer

British holidaymakers booking summer flights are flying with airlines at significantly different levels of protection against elevated fuel costs, according to new analysis published today by property intelligence platform My Flight Path.

The research scores ten major carriers on their fuel hedging coverage and schedule stability, finding that how well an airline has locked in its fuel costs across the full year - not just the summer peak - may be the single biggest factor separating carriers who are well insulated from continued fuel cost pressure from those with thinner protection against it.

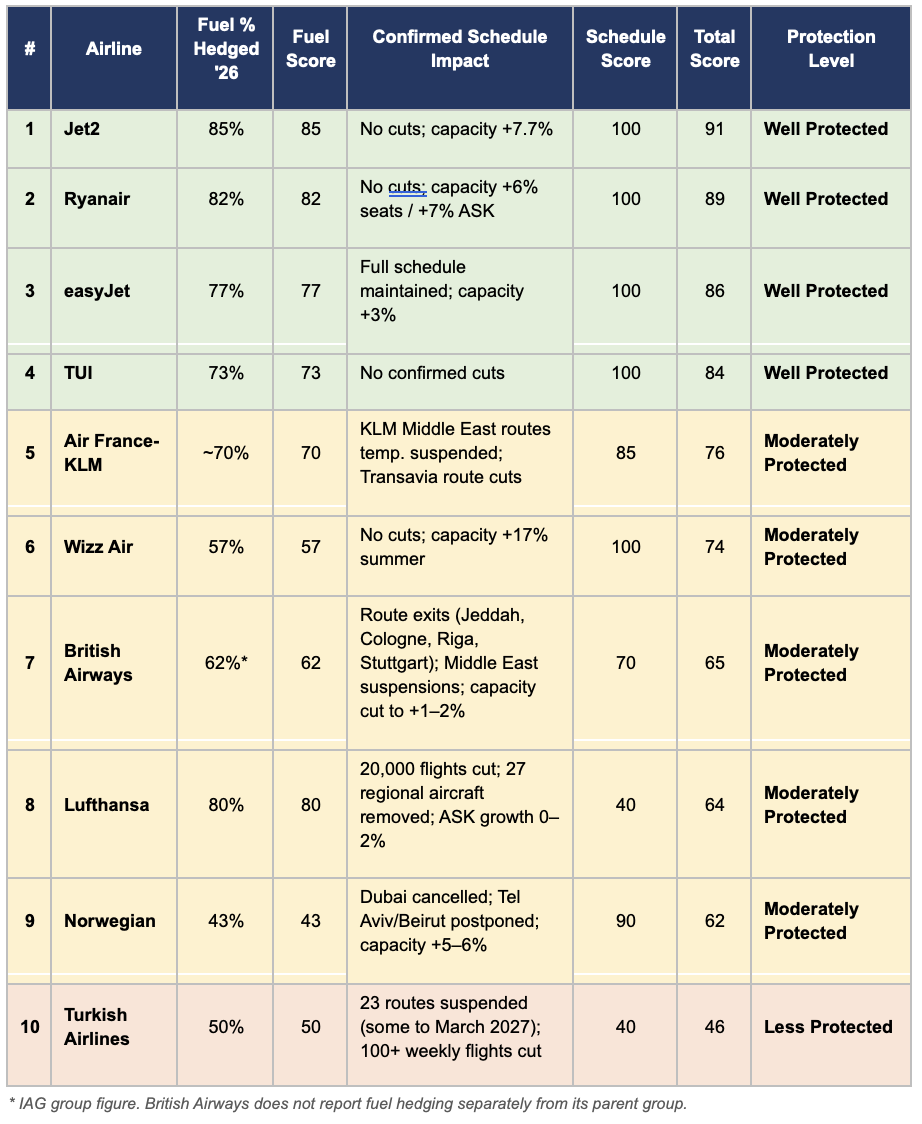

All data is drawn from the airlines’ own publicly available financial filings. Results show a significant spread: Jet2, rated top with a score of 91/100, has locked in approximately 85% of its 2026 fuel and Ryanair is close behind at 89/100, with approximately 82% of its 2026 fuel hedged. Turkish Airlines, at the foot of the index with a score of 40/100, has the lowest confirmed hedge coverage and has already suspended 23 international routes.

Jet fuel prices have risen from roughly $85–100 per barrel in late February to around $150–200 per barrel in some markets following disruption caused by the Iran conflict.

Fuel costs typically account for 20-30% of an airline's operating expenses in normal conditions. When prices remain elevated, how well an airline has locked in forward fuel prices - a practice known as hedging - can be the difference between a stable schedule and a season of difficult decisions.

The top tier: Britain's biggest leisure carriers lead the way

The most striking finding in this index is not which airlines come bottom, it is which ones come top. Jet2, Ryanair, easyJet and TUI, the four carriers operating more than half of all UK summer departures, occupy the top four positions and are all rated Well Protected. Between them they will carry the majority of British holidaymakers this summer, and on the measure that matters most this season - how much of their fuel cost is locked in - they are materially better insulated than several of the larger international network carriers below them.

What these airlines share is a systematic approach to fuel hedging that rarely features in coverage focused on baggage fees and leg room. All four have locked in the majority of their 2026 fuel requirements at rates well below current spot prices, and none has announced schedule cuts for the summer.

The risk of operating without adequate fuel protection is not hypothetical. US airline Spirit Airlines ceased all operations on 2 May 2026, leaving an estimated 600,000 passengers stranded and 17,000 workers without jobs. The airline had hedged none of its fuel for the year in which prices more than doubled.

Jono Oates, Co-Founder of My Flight Path, said: "The counterintuitive finding is that the airlines best known for cheap fares, rather than financial sophistication, turn out to be among the best protected this summer. Fuel hedging is unglamorous work, but right now it matters more than almost anything else an airline does.

"The gap between top and bottom of this index is wider than most would expect. Airlines with less fuel protection aren't necessarily going to cancel your flight, but they have a thinner cushion against further shocks. A second fuel spike, an operational disruption, a bad weather season: those things land very differently on a carrier with 85% of its fuel locked in than on one at 40%.

"People spend hours comparing fares before they book. This data is public - buried in annual reports that nobody outside the investment community reads. Translating it into something a family can check before they book is what this is about."

For passengers yet to book, fuel cost exposure increasingly feeds through into fares and ancillary pricing. Carriers with stronger hedging positions have more room to hold fares stable or even reduce them; those absorbing higher spot costs have less.

Airline analysis

1. Jet2 — 91/100 (Well Protected)

Jet2 does not typically feature in conversations about airline financial sophistication. Britain’s third-largest airline by passengers carries an outsized hedge book and a balance sheet that rivals carriers twice its size.

Jet2 has locked in approximately 85% of its 2026 fuel on a blended basis, with summer 2026 specifically covered at 87% at $707 per metric tonne - the highest confirmed summer coverage ratio in this index. As a predominantly summer leisure carrier, this figure effectively represents the airline’s core operating season. No schedule cuts have been announced; capacity is growing by 7.7%.

Source: Jet2 plc FY26 Preliminary Results, May 2026 (jet2plc.com/preliminary-results) — jet2plc.com/-/media/Jet2/Jet2plc/Jet2Plc_Redesign2025/Reports/2025/Jet2_PLC_Preliminary_Results_2025.pdf

2. Ryanair — 89/100 (Well Protected)

Ryanair’s brand is built on stripped-back fares and ancillary charges. What receives less attention is the treasury operation running behind it. The airline runs one of the most disciplined fuel hedging programmes in commercial aviation, using a rolling forward contract strategy that consistently locks in costs well below spot prices.

Ryanair has approximately 82% of its 2026 fuel hedged on a blended basis — 80% of its FY27 requirements (April 2026 onwards) locked in at approximately $67 per barrel ($528 per metric tonne), among the cheapest locked-in rates of any carrier globally. No schedule cuts have been announced; seat capacity is growing 6%.

Source: Ryanair Holdings Q3 FY26 Results, January 2026 — investor.ryanair.com/wp-content/uploads/2026/01/Q3-FY26-Ryanair-Results.pdf

3. easyJet — 86/100 (Well Protected)

easyJet runs a systematic hedging programme that covers both halves of the year, giving it a full-year blended position meaningfully ahead of many network carriers.

easyJet has 84% of its H1 2026 fuel hedged and 70% of H2, both at approximately $706 per metric tonne — giving a blended 77% for the full year. It carries £602 million in net cash and £4.8 billion in total liquidity and has confirmed no schedule cuts with seat capacity growing 3%.

Source: easyJet plc Trading Update, 16 April 2026 — cnbc.com/2026/04/16/easyjet-shares-fuel-costs-middle-east-bookings.html

4. TUI — 84/100 (Well Protected)

TUI’s score of 84/100 places it in the well protected tier, reflecting a strong fuel hedging position and an absence of confirmed schedule cuts — the two primary inputs to this index.

TUI has hedged 83% of its summer 2026 jet fuel requirement, tapering to 62% for Winter 2026/27 — giving a blended full-year coverage of approximately 73%. No schedule reductions have been confirmed for summer 2026.

The primary qualifier on TUI’s position is demand rather than supply: forward bookings for summer 2026 are running approximately 7% below the equivalent point last year, suggesting some softening of consumer confidence. This does not affect the airline’s fuel protection or its ability to operate its schedule as planned.

Source: TUI AG Q2 FY2026 Trading Statement, 15 April 2026 — tuigroup.com/en/investors/financial-news/tui-adjusts-fy-2026-underlying-ebit-guidance-at-constant-currency-due-to-the-continuing-iran-war

5. Air France-KLM — 76/100 (Moderately Protected)

Air France-KLM enters summer with a stronger financial position than its score might initially suggest. The group holds €10.6 billion in total liquidity as of Q1 2026 — above its own target range of €6–8 billion — and generated €884 million in positive operating cash flow in Q1.

The moderate score reflects a hedging position that declines steeply through the year. Air France-KLM has disclosed a blended full-year 2026 coverage of ~70%, but the quarterly profile is uneven: approximately 70% in Q1–Q2, falling to 60% in Q3 and 50% in Q4. The Q2 effective price is $1,260 per metric tonne — significantly above levels locked in by the UK low-cost carriers. An additional $2.4 billion fuel cost exposure in 2026 has driven operational adjustments: KLM has suspended Middle East routes through May and made reductions to its Transavia subsidiary, though mainline Air France’s schedule has been broadly maintained.

Source: Air France-KLM Q1 2026 press release, 30 April 2026 — globenewswire.com/news-release/2026/04/30/3284465/0/en/Q1-2026-press-release.html | Results presentation: airfranceklm.com/sites/default/files/2026-04/afklm_q1_2026_results-presentation.pdf

6. Wizz Air — 74/100 (Moderately Protected)

Wizz Air’s score of 74/100 places it at the top of the moderately protected tier. Its summer 2026 fuel position is stronger than its full-year figure suggests — the airline has publicly confirmed 70% summer coverage at approximately $700 per metric tonne — but the blended full-year FY27 position (covering April 2026 onwards) is approximately 57%, reflecting lower coverage in the second half of the year.

On schedule, Wizz Air is one of the most expansionary carriers in this index: summer 2026 capacity is growing by approximately 17%, driven by its Central and Eastern European network. No route cuts have been confirmed.

The financial context warrants noting: a €50 million profit warning was issued in April 2026, with full-year guidance pointing to effectively breakeven profitability. Morningstar has assessed Wizz Air as carrying the lowest margin buffer of any carrier in this index. These factors do not affect the scored components — fuel hedging and schedule stability — but they indicate that the airline’s operational delivery has less financial cushion behind it than the score alone reflects.

Source: Wizz Air Q3 FY26 Results, January 2026 — wizzair.com/cms/api/docs/default-source/downloadable-documents/corporate-website-transfer-documents/results-and-presentations/wizz-air-holdings-plc---f26-q3-report_2025-12-31.pdf | Schedule: enginecowl.com/wizz-air-uk-expansion-s26

7. British Airways — 65/100 (Moderately Protected)

IAG, British Airways’ parent group, reported Q1 2026 operating profit up 77% to €351 million despite an expected €2 billion increase in full-year fuel costs — a result the group attributed in large part to its hedging programme and fare recovery.

British Airways’ score reflects a hedge position that weakens materially through the year. The IAG group is 75% hedged in Q1, falling to 64% in Q2, 58% in Q3 and 50% in Q4 — a blended annual figure of approximately 62%. Note that fuel hedging is reported at IAG group level; British Airways does not disclose its position independently. The 70% ‘rest of year’ figure cited in some group disclosures refers to the post-Q1 period only and overstates the full-year blended coverage.

On schedule, British Airways has made more substantial adjustments than many carriers in this index: permanent route exits from Jeddah, Cologne, Riga and Stuttgart; temporary suspension of Dubai, Amman, Bahrain and Tel Aviv services through May; and overall capacity growth reduced to +1–2%.

Source: IAG Q1 2026 Results, 8 May 2026 — rns-pdf.londonstockexchange.com/rns/4939D_1-2026-5-7.pdf

8. Lufthansa — 64/100 (Moderately Protected)

Lufthansa’s score illustrates a distinction this index is designed to capture: the difference between fuel protection and schedule resilience. With approximately 80% of its 2026 fuel hedged on a blended basis — among the highest ratios in this index — Lufthansa is meaningfully insulated from the worst fuel price scenarios. Yet its score sits near the bottom of the moderately protected tier.

The scale of the fuel cost increase — an additional €1.7 billion in 2026 despite that hedging — has driven substantial schedule action. Lufthansa is removing 27 CityLine regional aircraft from its schedule, early-retiring A340-600s, and grounding some 747-400s. Overall ASK growth has been cut from a planned 4% to 0–2%, with approximately 20,000 flights removed from the 2026 network. Named permanent route exits include Bydgoszcz, Rzesżów and Stavanger; short-haul services from Frankfurt and Munich have been significantly thinned.

Passengers on affected short-haul and regional routes should check whether their specific service is among those already removed from the schedule. Those on Lufthansa’s long-haul network are largely unaffected, as the capacity reductions are concentrated in lower-margin short-haul flying.

Source: Lufthansa Group Q1 2026 Results, 6 May 2026 — newsroom.lufthansagroup.com/en/lufthansa-group-significantly-improves-operating-result-in-first-quarter-and-maintains-positive-full-year-outlook | 20,000 flights: aljazeera.com/news/2026/4/23/lufthansa-cuts-20000-flights-as-iran-war-causes-jet-fuel-shortage

9. Norwegian — 62/100 (Moderately Protected)

Norwegian enters the season with approximately 43% of its 2026 fuel hedged on a blended basis — among the lowest ratios in this index. Q2 specifically is 42% covered at $679 per metric tonne, with the second half at around 43% and 2027 at just 22%. It is the airline’s low hedge ratio — not its schedule — that places it near the bottom of the moderately protected tier.

On schedule, Norwegian’s picture is more positive: summer 2026 capacity is growing by 5–6%, with the airline’s principal confirmed changes limited to the cancellation of its Dubai service and the postponement of planned Tel Aviv and Beirut routes. Q1 2026 operating results showed genuine progress, with the operating loss improving to NOK −220 million from NOK −611 million in the prior year, supported by hedging gains, a record Q1 load factor of 87.6%, and a 22% fall in fuel costs year-on-year.

Source: Norwegian Air Shuttle Q1 2026 Results, 28 April 2026 — rte.ie/news/business/2026/0428/1570552-norwegian-air-quarterly-results

10. Turkish Airlines — 46/100 (Less Protected)

Turkish Airlines presents a mixed picture. The carrier posted a strong Q1 2026: revenue of $5.9 billion (+21% year-on-year) and net profit of $226 million — one of the best quarterly performances among the airlines in this index. It benefits from state backing and a large, young fleet averaging 9.8 years.

However, Turkish Airlines has suspended 23 international routes and cut over 100 weekly flights from May 2026 — the largest network reduction of any carrier in this index. Some African routes, including Juba, Kinshasa and Luanda, are suspended to March 2027, making these effectively multi-year withdrawals rather than temporary measures. Turkish Airlines does not publish granular hedging data, but management confirmed in the Q1 2026 earnings call that the airline is hedging approximately 40% of fuel consumption and is not continuing its regular hedging policy — adding contracts opportunistically rather than through systematic forward coverage.

Source: Turkish Airlines Q1 2026 Results (aerohaber.com, May 2026); route suspensions